최근 글 목록

-

- 2021/05/15

- ou_topia

- 2021

-

- 2021/03/10(1)

- ou_topia

- 2021

-

- 2021/03/09

- ou_topia

- 2021

-

- 2021/03/08

- ou_topia

- 2021

-

- 2021/02/06

- ou_topia

- 2021

Solidarity and Cohesion within and between

Countries in a Europe in Crisis

Andrew Watt

출처:http://www.bertelsmann-stiftung.de/bst/de/media/xcms_bst_dms_35357_35358_2.pdf

This essay considers how Europe has performed prior to and during the ongoing financial and economic crisis in terms of cohesion and solidarity, both within and between countries. The linkages between within-country (or „social‟), and between-country (or „European‟) cohesion and solidarity are also examined.

For the limited purposes of this essay, the terms solidarity and cohesion are used quite loosely to refer to a situation in which market outcomes are influenced and corrected by means of policies and institutions in a way that reduces the income and other welfare differentials between rich and poor, either at the national or the European level. Cohesion is an outcome of such a process. Solidarity is, if you like, the driving force: the belief that aggregate human welfare is increased if resources are shared more equally and, especially in difficult times, if the strong shoulder a proportionately greater share of the burden. Solidarity and cohesion are considered normatively „good things‟, although practical and also ethical limits to such solidarity will be discussed.

It is argued that, prior to the crisis, the growth model adopted by individual European countries, and by the European Union as a whole, was inimical to social cohesion and solidarity, but that there was a general trend towards greater cohesion across national borders (i.e. a convergence of economic welfare indicators) and some limited degree of international solidarity (i.e. in terms of processes, institutions). In the crisis, social cohesion initially increased; this trend was superficial and short-lived, however. The medium-term outlook for social cohesion is bleak because the previous growth model has been largely left intact while the pressures of crisis adjustment have not been distributed according to the principle of solidarity. Inequality within countries is set to rise.

At the same time, as the crisis proceeded the process of convergence between countries largely came to an end, certainly within the euro area, giving way to growing divergence. The crisis has been accompanied by what may appear to have been an increase in cross-border solidarity, with the establishment of bail-out funds, the European Financial Stability Facility (ESFS), and a debate about introducing euro bonds. On the other hand, there has been much talk about the supposedly „natural‟ limits to solidarity between EU countries – essentially the old idea that Europe lacks a demos – and there have been clear signs of resistance to „helping‟ peripheral countries on the part of citizens in „core Europe‟.

However, it is argued here that the debate has been largely conducted on false premises. The competitiveness (and resultant sovereign debt) problems in the euro area are „symmetrical‟. Deficits in one country automatically imply surpluses in another. What is needed is not so much what might be called „uni-directional conditional solidarity‟ (i.e. bail-outs subject to tough conditionality) as symmetrical adjustment behaviour by both surplus and deficit countries, plus changes at the European level that are not so much about introducing „solidarity‟, as is commonly perceived, but rather more about ensuring the efficient functioning of a monetary union.

At the time of writing, this needed shift in policy does not seem likely. And the perceived – but actually misconceived – „limits to cross-national solidarity‟ threaten to destroy monetary union and perhaps lastingly damage the whole idea of a Europe based on cohesion and solidarity.

Pre-crisis growth model built on growing inequality

As charted by a number of studies, perhaps most comprehensively by the OECD‟s Growing Unequal report (OECD 2008), the growth model characteristic of European countries (and even more so in much of the non-EU OECD) has been based on widening social inequalities since the early 1980s. This was in contrast to the post-war period up until the late 1970s, in which most measures of inequality were declining.

The declining social cohesion was not limited to incomes. While economic growth was employment intensive, there was a hollowing out of middle-class jobs and a rise in the „precariat‟: people working on bad jobs and under insecure employment contracts. In Spain around a third of people were employed on fixed-term contracts, the vast majority involuntarily. The opening up of the bottom third of the labour market was particularly pronounced in some countries – in Europe most notably in Germany, which went from being a rather equal country to one that, on some measures, was as unequal as the „liberal' United Kingdom (on rising inequality in Germany see Horn 2011). In many countries, public services were increasingly also

provided on 'market principles', reducing their market-correcting impact. In most countries, average wage growth failed to keep up with productivity growth so that the share of wages in national income decreased, while that of profits increased. In the twelve founding European Monetary Union (EMU) member countries, for instance, the wage share fell from around more than 68 percent of GDP in the early 1990s to 63 percent

when the crisis hit. Moreover, the wage share includes some categories of incomes, notably stock options, which have expanded very rapidly in recent decades and accrue to a small share of the population consisting of CEOs and senior management personnel. These incomes would, in a more intuitive classification of the share of 'wages' and 'profits' in national income, be at least in part classified under profits, implying that the real fall in the wage share is considerably greater than implied by the national accounts (Atkinson 2009, Glyn 2009).

The factors driving this inequality-based growth model are disputed and hard to disentangle. There is some agreement that globalisation (against the background of the higher mobility of capital compared to labour) and socalled „skill-based‟ technical change have contributed to rising inequalities, but not about their importance. A shift to greater „financialisation‟ of economies (particularly in English-speaking countries) is put forward by a number of authors as an important factor (e.g. Hein 2011). Institutional changes, such as de-unionisation (O‟Farrell/Watt 2009) and „reforms‟ of welfare states and labour market institutions, are also emphasised to varying degrees (OECD 2011).

It is not necessary here to apportion „blame‟ between these factors, merely to note more generally that the decline in social cohesion in the period since 1980 was an expression of a liberal and globalised growth

model, based not least on the idea of competition between (welfare) states and wage levels in different countries. This was in marked contrast to the prior social (or Christian) democratic growth model of shared prosperity under which welfare states played primarily a protective and corrective function, and the double function of wages as both cost factor and source of demand was recognised.

Nor will we dwell here on the question whether the growing inequality was, in turn, an important cause of the crisis of the global 2007. (On this see among many others: Coats 2011, Horn 2011, Rajan 2010, Watt 2009.) What is certainly clear is that the growth model came to a juddering halt in Europe, and globally, starting in 2007, just as some 80 years earlier the Great Depression ended the turbulent post-1918 growth model that had also been characterised by widening social inequalities (Picketty/Saez 2006).

On the other hand, the years after the founding of the euro in 1999 and after the eastern enlargements in 2004 and 2007 did see an appreciable convergence of income levels between European countries (Figure 1). The south and east (and Ireland in the west) – in short the European „periphery‟ – grew faster than the northern and central „core‟. Social divergence went hand in hand with international convergence within Europe. While the latter partly reflected standard economic mechanisms, such as trade and capital and labour mobility, it was also a manifestation of European cross-border solidarity: the cohesion funds and other elements of support made a limited but nonetheless significant contribution to the convergence process. This convergence process can count as an important success for the European integration project, all the more so as it does not appear to have occurred in other regions of the global economy (Gill/Raiser 2011).

However this apparently very successful story of convergence concealed worrying underlying trends that stored up problems for the future. The most important of these was the increase in current account deficits

and rising price and wage uncompetitiveness in the peripheral countries, and corresponding current account surpluses and increasing wage and price competitiveness in the core countries, especially Germany.

As a proper understanding of this dynamic is important for the subsequent discussion, it is necessary to dwell for a moment on this issue. We focus on the euro area.

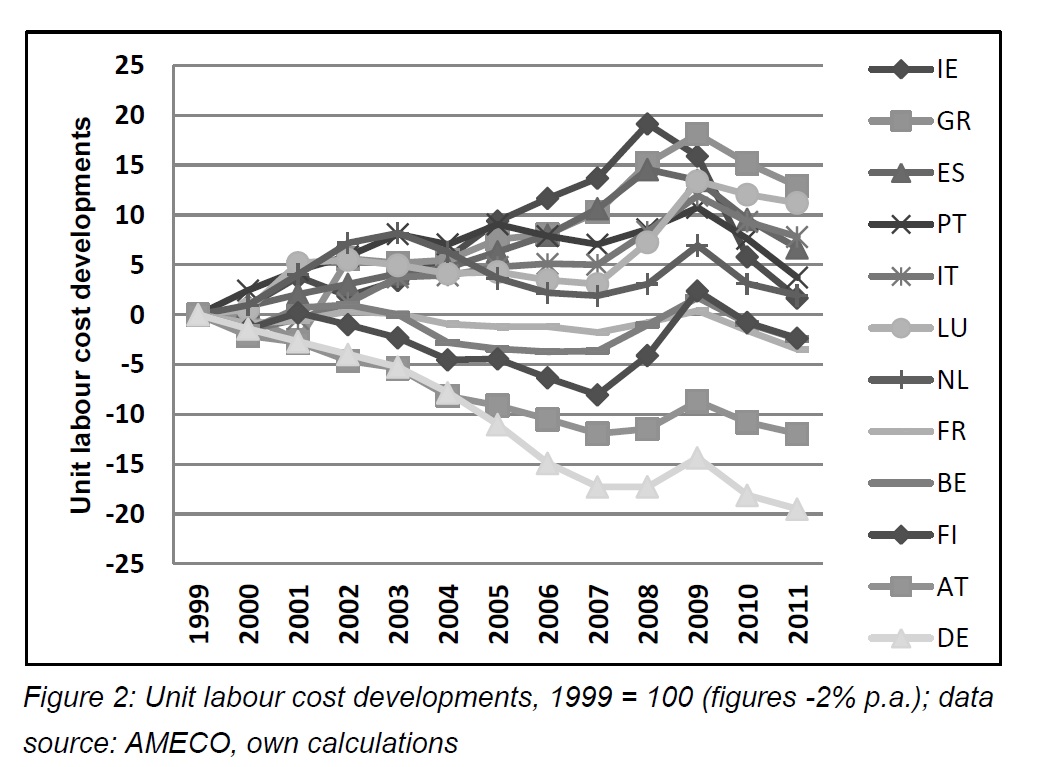

First of all there is a clear correlation between the development of unit labour costs – that is nominal wage growth minus labour productivity growth – and developments in current account balances. This can be seen by comparing Figures 2 and 3 for the EMU countries. In layperson‟s terms and simplifying somewhat: countries in which labour costs rose substantially faster than productivity tended to import more than they exported. Countries in which wages increased more slowly, allowing for their national productivity trends, tended to run export surpluses.

(단위노동비용 GR가 그리스, DE가 독일)

The link between these two developments is complex, however. In particular, the correlation does not permit the conclusion – as many have erroneously claimed – that irresponsible wage policy in the periphery has been at the root of the euro area crisis. In a nutshell the developments can

be explained as follows.

On joining EMU, previously high-inflation countries, which had had high interest rates, benefited from a sharp fall in borrowing costs, setting off a – seemingly – virtuous circle: these fast-growing, high-inflation economies enjoyed relatively low real interest rates (the common ECB-rate minus their high inflation rates), which stimulated growth further. On the other hand, slow-growing, low-inflation countries were in a vicious circle, suffering from relatively high real interest rates, which were a drag on growth. This dichotomy was exaggerated by the one-sided nature of the Stability and Growth Pact: slow-growing economies were up against or over the 3 percent of GDP deficit limit and prevented from pursuing expansionary fiscal policies, while faster-growing economies were not constrained to run tighter policies.

Asset (especially house) prices rose rapidly in the peripheral countries, thanks to low interest rates, creating wealth and confidence effects that stimulated spending and borrowing. But it wasn‟t just a financial bubble.

Employment growth was strong – Spain created around one third of all the net jobs created in the euro area up to 2007 – and unemployment fell significantly in peripheral countries. By contrast Germany‟s labour market performance was extremely weak during the pre-crisis EMU period, a fact that is now often overlooked.

This led to a situation of sustained nominal wage/price „spirals‟ – where wages and prices chase themselves upwards – that twisted faster in some countries, the periphery, than in others, the core. The combination of fasterrising prices and a stronger dynamic of domestic demand in deficit countries

restrained their exports while fuelling import demand; the reverse happened in surplus countries. In Germany domestic demand was essentially stagnant – as were real wages – and such economic growth as it achieved was driven solely by higher net exports.

Because running persistent current account deficits means that a country steadily increases its foreign indebtedness, the seemingly good performance of the periphery was too good to be true. From around 2007 foreign lenders became nervous about debt repayment. Capital inflows stopped. Bubbles burst and growth ground to halt.

One vital point needs to be grasped from Figures 2 and 3. The unit labour cost problem in the euro area is a symmetrical one. Some countries exceeded the benchmark rate of unit labour cost growth, which is 2 percent per annum, equal to the inflation target of the European Central Bank (ECB). But others undercut it. (While more countries exceeded than undercut, the size of Germany, representing 30 percent of euro area GDP, relative to Spain, Greece, Ireland and the rest, needs to be borne in mind.) Similarly the current account imbalances more or less netted out. This is unsurprising given that the external trade balance of the euro area as a whole has, for many years, been very close to balance. Thus deficits in one EMU country are a necessary, equal and opposite, corollary of surpluses in other countries.

Direct impact of the crisis on social cohesion and international

Convergence

The initial effect of the crisis was to narrow social inequality. This was not due to any increase in solidarity, however, but was rather a statistical expression of the fact that top incomes, profits, and not least financial-sector bonuses were hit first and hardest, whereas the wages of those workers who kept their jobs, as contractual income, were initially maintained, while most of those that lost their jobs were initially entitled to some welfare benefits; to a limited extent the latter were stocked up or extended as part of the anti-crisis stimulus packages that, belatedly, were rolled out (Watt 2009a). The share of wages in national income, which had been on a steady downward trend, picked up.

Not only was this „improvement‟ in social cohesion more of a statistical mirage – incomes at the bottom fell less than at the top as the crisis hit – it was, or, depending on country and indicator, is likely soon to prove,

temporary. Rising unemployment increases inequality amongst workers, with big income losses for some, especially as unemployment duration increases and benefit entitlements run out. More generally, higher

unemployment weakens the bargaining power of labour presaging a renewed fall in the wage share, especially for those groups with already weak bargaining power (the unskilled, migrants, those in depressed areas with limited mobility).

On top of this, the crisis brought to an abrupt end, and shows signs of reversing, the sustained process of international convergence within Europe. The crisis disproportionately hit the „peripheral‟ countries of eastern and southern Europe, and Ireland, whereas Germany and most of the core countries around it tended to weather the crisis relatively well (Figure 4). This largely reflected the fact that, as detailed below, the peripheral countries had to cope not only with the fall-out of the global crisis, but also with the need to regain competitiveness.

(...)

Andrew Watt is a Senior Researcher at the European Trade Union

Institute, where he coordinates research on economic, employment, and

social policies. He edits the ETUI Policy Brief on economic and employment

policy, coordinates the European Labour Network for Economic Policy, and

writes a column for the Social Europe Journal. He has worked as a

consultant/adviser to the European Commission, Eurofound, and the

European Economic and Social Committee.

| 2021/05/15 |

| 2021/03/10 |

| 2021/03/09 |

| 2021/03/08 |

| 2021/02/06 |

최근 댓글 목록